State of Logistics 2020: Managing the Supply Chain in a Changed World

With the transformation of the supply chain wrought by the Coronavirus pandemic, logistics services customers are going to require from their providers increased agility, financial stability, transparency and speed—and some are seriously considering insourcing at least some of those services.

That is the conclusion of researchers and company executives who contributed to the 2020 State of Logistics Report issued in June by the Council of Supply Chain Management Professionals (CSCMP). The report was sponsored by Penske Logistics and the research was performed by the Kearney consulting firm.

“It is abundantly clear logistics have a driving role in assuring resilient supply chains,” declares Michael Zimmerman, partner with Kearney and co-author of the 2020 report. “Logistics practitioners will need to become even more agile as they navigate recovery in the second half of 2020 and into 2021.”

According to Marc Althen, president of Penske Logistics, “With the reopening of American businesses, many supply chains have become off-balance. Supply chain managers must rely on solid data and experienced advice as they move forward. This is an important time to reevaluate your supply chain, from distribution points to modes of transportation.”

Rick Blasgen, president of CSCMP, agrees. “To say that everything changed is an understatement. Many in our industry have led efforts in adapting, innovating and managing through unprecedented disruption while simultaneously creating new operating models.” The three keys to being prepared for the future, he says, are being able to adapt, improvise and overcome.

When the State of Logistics Report was first created more than three decades ago, its main purpose was contributing to the policy debate over economic deregulation of trucking by measuring the positive impact deregulation had on logistics costs over the previous year. After several years of proving the beneficial effect of deregulation on costs, the report added more data about other modes and services.

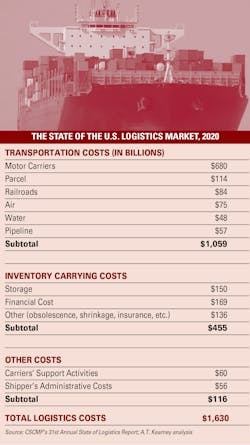

In recent years that focus has shifted to providing more of an outlook for what is expected to happen to the industry, while continuing to analyze the previous year’s performance in various sectors. The 2019 report found that U.S. business logistics costs in general last year rose 0.6% to $1.63 trillion, or 7.6% of 2019’s $21.43 trillion GDP. Compared to the 7.9% of GDP in 2018, this reflected achievement of better productivity overall.

That seems like ancient history now. The economic slowdown seriously impacted most of the economy, including logistics. Even before COVID-19 hit, a slew of truckload haulers had begun declaring bankruptcy. Some shippers now face higher rates, while others are greeted by over-capacity.

“To get through trying times, all parties will need to make smart investments in technology and use such technologies to deepen collaboration,” the Kearney researchers state. “Supply chains will need to become more resilient, better able to adjust to and recover from future difficulties. The shift away from single-source, cost-focused supply functions may pose new challenges to logistics—which itself is having its resilience tested in this crisis.”

Mixed Picture for Providers

Most freight in the U.S. is transported at least at some point by trucks. Trucking was already slowing down in 2019 after a torrid 2018, the report notes. After two years of scarce capacity and increasing rates, the 2019 market balance tipped in favor of shippers. They regained buying power and were able to negotiate lower rates and secure capacity.

At the same time, fleets experienced reduced profits and ended up ordering fewer new trucks. Beyond the resumption of a boom-and-bust cycle now exacerbated by COVID-19, big carriers are turning to technology investments that promise to increase efficiency, while others are staring into the abyss.

On June 30—a week after the CSCMP report was published—the federal government loaned $700 million under the CARES Act to less-than-truckload (LTL) carrier YRC in exchange for a 29.6% equity stake in that Teamsters union employer.

Small fleets will need to scramble to survive, the Kearney researchers assert. “Smaller carriers, especially those in highly affected industries, must look to app-based solutions and brokers to provide access to better fit routes and backhauls.”

Railroads continued to grow profitability despite declining 2019 volumes, which was largely the function of having pushed costs onto their shippers in recent years through the adoption of Precision Scheduled Railroading (PSR), and by changing demurrage and accessorial fees to turn into a revenue stream by monetizing the inefficiencies the railroads created themselves.

However, the COVID-19 pandemic slashed volumes by another roughly 25%, and railroads face high fixed costs to maintain their networks in their core carload business. To generate more revenue, the major freight railroads are looking again at intermodal, which they had treated like the proverbial red-headed stepchild during their rush to embrace PSR.

Given intermodal’s cost and carbon-footprint benefits, shippers are keen for better prices and reliability. According to the researchers, the railroads have taken notice of this, and say they are working on ways to improve their intermodal networks.

On the other side of the intermodal equation, ocean shipping saw volumes soar in 2018 in anticipation of U.S. tariffs, but both in 2019 and this year the industry has managed to find new sources of pain. Shippers found they had entered 2019 with excess inventory that reduced their ocean shipping needs, and ocean carriers were hit with new and expensive environmental regulations.

In the wake of COVID-19, additional financial strain is likely to continue well into the future. “Ship and container imbalances and capacity uncertainty have driven up spot-market prices and suspended normal contracted rate negotiations as the demand picture remains clouded,” the researchers explain.

U.S. ports began 2020 by enjoying growing shipment volumes and improving efficiencies, but the pandemic soon left them reeling as they had to deal with dropping volumes, congestion and hundreds of thousands of boxes stranded at terminals.

Expect Warehousing Growth

Last year, warehouse rents continued rising and vacancy rates stayed near historic lows. E-commerce continued to drive growth, especially in regard to smaller, high-amenity urban warehouses operating closer to the customer base, the report notes.

Inventory storage costs grew 6.6% in 2019 because warehousing capacity remained tight, which in fact has been the case for many years, although the pace of construction also increased. “Warehouses delivered the highest square footage completed in a single quarter on record—and the market quickly swallowed it up,” the Kearney researchers report.

In 2020, the researchers expect that disruption of consumer supply chains stemming from the Coronavirus pandemic will drive a new surge in warehousing demand, especially for temperature-controlled warehouse space as more consumers order food online. But that won’t be the only driver.

The researchers estimate that a 5% bump in safety-stock inventory will require about 750 million square feet of additional industrial space as companies soften their former lean-inventory strategies, such as Just-in-Time and Quick Response.

“The rise in stock levels should spur industrial activity, given the expectation that the warehouse construction pipeline will remain full and warehouse availability will remain tight,” they predict.

These trends demand greater attention to efficient management of both private warehouses and companies providing third-party logistics (3PL) warehouse services, which help customers manage other supply chain needs by providing trucking, freight brokerage, freight forwarding, packaging and materials handling, along with other specialized services.

Technology is also being deployed to boost efficiencies in both warehouses and distribution center operations. “Pandemic e-commerce is leading to an expected increase in adoption of warehouse automation solutions to keep costs and operational complexity in check even further,” the researchers explain.

Sales of autonomous mobile robots are estimated to double to $27 billion by 2025, they point out. This and other tech solutions put the industry in a good position to support a vigorous recovery.

Building on Logistics’ Success

The pandemic tested 3PL service providers without warning, confronting them with sudden stops and surges, depending on which industries they served, and this is expected to have lasting effect. Most heavy manufacturing, the automotive industry and important segments of basic chemicals came to a stop when factories closed because demand had evaporated.

“The 3PLs and supply chains serving the hospitality and restaurant industries were mostly stopped cold,” the report says. “On the other hand, high-tech products such as microprocessors continued to fly across the globe, still needed for providing inputs to crucial computers, servers and military products.” In addition, consumer packaged goods and grocery demand surged as people hoarded and then shopped while adhering to shelter-at-home orders.

The report remarks that a number of 3PLs were able to redeploy some of their people and assets from the halted and slowed industries to the ones that experienced surges. “Most shippers we spoke with reported that their 3PLs had a ‘we’re in this together’ attitude rather than invoking force majeure clauses,” the researchers reveal.

However, the report’s authors warn that 3PLs need to keep investing in technology and sharpening their expertise. “Some shippers told us that advances in technologies (warehouse management systems, transportation management systems, track and trace) make the insourcing decision easier to take.”

They add, “Those shippers committed to buying talent and innovation from 3PLs reported that they were seeing incremental improvements in creativity, such as the campus model for 3PLs where multiple shippers are served from the same group of facilities, or the buildup of 3PL last-mile networks and extra cross-dock capacity that can help shippers with surges.”

The impacts of the COVID-19 crisis have opened the eyes of customers and providers alike to the value of technology in supply chain management, the researchers stress. “Even providers previously hesitant to invest in shipment location tracking or electronic signatures, claiming such digital technologies were unnecessary, are now embracing them as table stakes.”

With rising labor costs, and despite the COVID-19-induced recession, shippers and 3PLs look to automation and robotics to make logistics more efficient—not just by achieving control over complex and unpredictable product flow, but also by helping gain greater control over labor costs.

While the Kearney researchers believe that serious growth and application of autonomous trucking is still five to 15 years away, they note that legions of mobile robots are already working alongside humans in many warehouses and DCs.

The logistics industry had exhibited very good fundamentals before the pandemic devastated the economy, and those will help it weather the current storm, the researchers claim. “Although almost nobody saw the COVID-19 crisis coming, the state of the industry in 2019 suggests that it could recover quickly.”

They contend that the rapid deployment of professional skill and quick actions taken to find creative solutions by logistics professionals on display from the early stages of the pandemic should bode well for the future of the industry.

“Logisticians rolled up their sleeves instead of hiding behind their contracts. People across the industry—indeed, across the world—are coming together to face this dramatic crash and rebuild from it. Players in the logistics industry are seeing the rewards of collaboration, which now motivate them to go further with bold new solutions.”

The researchers summarize their view: “In general, winners will emerge from this crisis with more digitally savvy logistics operations, especially in the areas of creating transparency and interfaces while reducing needs for physical labor across modes and nodes.”

David Sparkman is founding editor of ACWI Advance, the newsletter of the American Chain of Warehouses Inc., as well as a member of the MH&L Editorial Advisory Board.

About the Author

David Sparkman

founding editor

David Sparkman is founding editor of ACWI Advance (www.acwi.org), the newsletter of the American Chain of Warehouses Inc. He also heads David Sparkman Consulting, a Washington D.C. area public relations and communications firm. Prior to these he was director of industry relations for the International Warehouse Logistics Association. Sparkman has also been a freelance writer, specializing in logistics and freight transportation. He has served as vice president of communications for the American Moving and Storage Association, director of communications for the National Private Truck Council, and for two decades with American Trucking Associations on its weekly newspaper, Transport Topics.