Supply Chain Cost to Rise 2.3%-4% Above Inflation

Driven by structural forces in trade policy, critical minerals constraints, geopolitical friction, and elevated inventory levels that persist even as container rates and commodity prices moderate, supply chain costs will rise in the range of 2.3% to 4% above inflation through 2026. This is the prediction of the Supply Chain Navigator, 2026 H1 Briefing from Kearney.

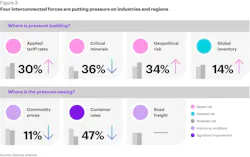

Applied tariff rates

Across major economies, including China, Germany, the United States, and India, average tariff levels have risen by roughly 30%, driven by industrial policy, trade restrictions, and security considerations.

Tariffs have shifted from predictable trade friction to tools of geopolitical strategy, shaped as much by security and political considerations as by economic policy, creating cost pressure that persists even in the absence of formal policy changes.

Direct costs add up. Applied tariffs raise landed costs on affected goods—material and difficult to offset for organizations with large cross-border flows.

Policy uncertainty premiums compound. Organizations build inventory ahead of anticipated policy shifts, diversify supply bases, and structure contracts to manage tariff risk, increasing carrying costs and contractual complexity.

Tariffs embedded in planning. In earnings commentary and internal planning, manufacturers increasingly treat tariffs as part of the baseline cost structure, incorporating exposure directly into pricing decisions, cost baselines, and inventory valuation.

Compliance burden. Expanding trade controls, origin requirements, and reporting obligations add administrative cost that compounds in complex global networks.

Tariffs now operate as a standing cost in enterprise planning. Organizations that plan for them absorb pressure earlier.

Critical minerals

Global exports of critical minerals have decreased by more than a third over the past year.

Analysis from the World Economic Forum supports this, noting that access to these materials is increasingly shaped by state control, export restrictions, and strategic stockpiling rather than by market-clearing mechanisms.

Concentration creates access risk. Processing capacity is concentrated in a small number of geographies where a single country often controls a large share of global refined output. Supply may remain available, yet access can be constrained by export controls, priority allocation, or price volatility driven by strategic considerations.

Volatility without interruption. Materials continue to move through established supply channels, while pricing increasingly reflects policy direction, geopolitical tensions, and long-term access security rather than near-term supply-and-demand conditions.

Exposure remains difficult to see. For many organizations, exposure exists in several tiers removed from subcomponents and production inputs that are not sourced directly. Exposure is often recognized only when cost, capacity, or delivery is already affected.

Demand drivers compound concentration. Electric vehicles, renewable energy, consumer electronics, and defense applications rely on many of the same critical minerals, concentrating demand pressure on a limited set of supply sources.